.png)

The Ultimate Guide to Workers Compensation Insurance in Massachusetts: Everything You Need to Succeed

- Ginette Preto

- Feb 18

- 5 min read

Massachusetts doesn't mess around when it comes to workers compensation insurance. If you employ even one person in the Bay State, you need coverage, period. No loopholes, no "I'll get to it later," no gray areas.

And the penalties for skipping it? Let's just say they're expensive enough to make your accountant cry.

Whether you're launching your first small business or managing a growing team, understanding workers compensation insurance in Massachusetts isn't optional. It's the law. But it's also your safety net, protecting both your employees and your business when accidents happen.

Here's everything you need to know to stay compliant, protect your team, and avoid costly mistakes.

Who Actually Needs Workers Comp in Massachusetts?

Short answer: Almost everyone.

Massachusetts has some of the strictest workers compensation requirements in the country. If you have employees, you need coverage. It doesn't matter if they're:

Full-time or part-time

Seasonal or temporary

Interns (yes, even unpaid ones)

Family members working in your business

Domestic workers putting in 16+ hours per week

You're required to carry workers compensation insurance Massachusetts coverage from day one, no "wait until I have five employees" grace period.

The Few Exceptions

Only a handful of situations get you off the hook:

Sole proprietors with zero employees (just you running the show)

LLC members who file proper opt-out documentation with the state

Officers who own at least 25% may exempt themselves. *They must file Form 153 with DIA.

Certain taxi drivers and real estate agents working as independent contractors

Domestic employees working fewer than 16 hours weekly, unless the employer elects coverage.

If you don't fall into one of these narrow exemptions, you need coverage. No debate.

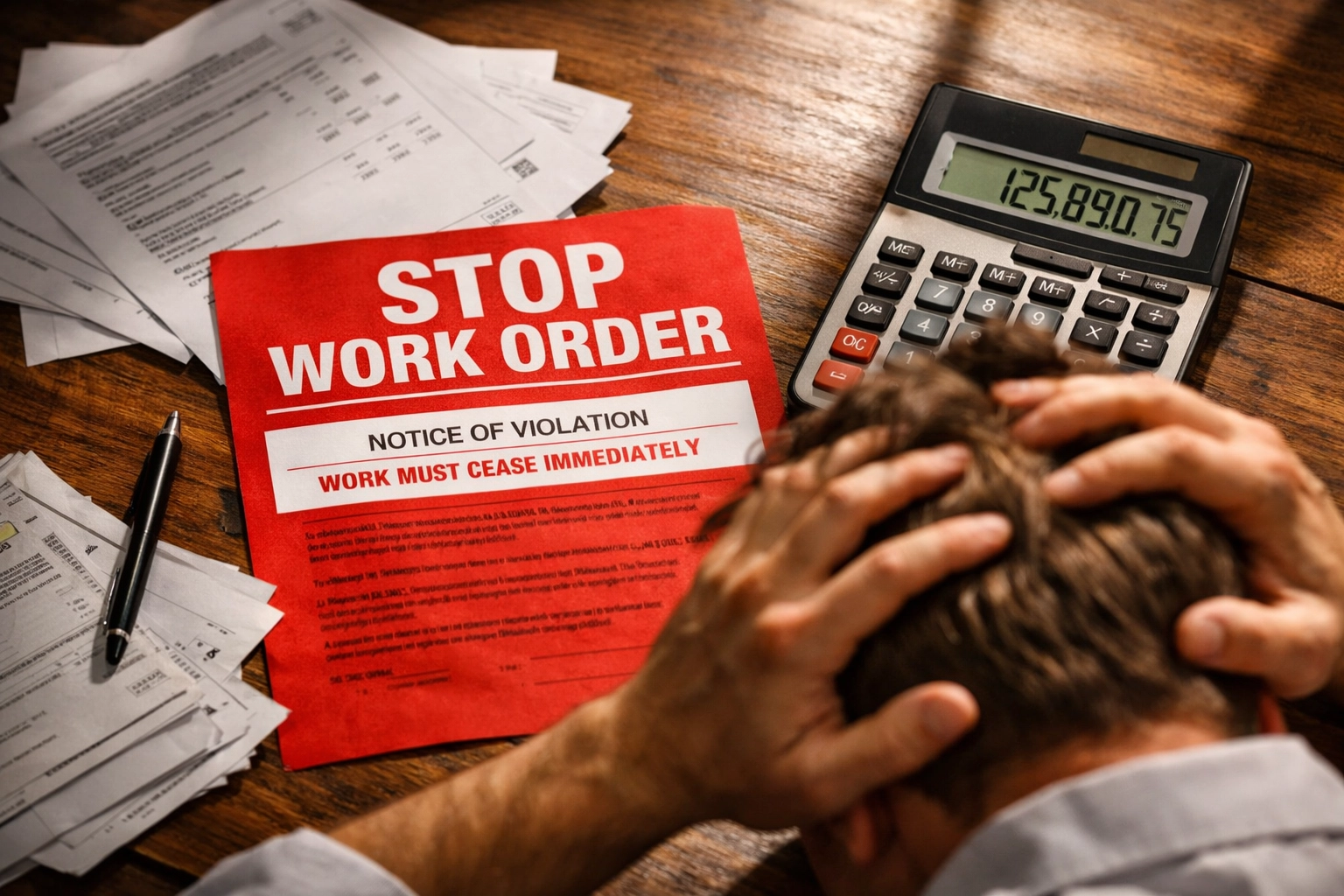

What Happens If You Skip Workers Comp? (Spoiler: It's Bad)

Massachusetts doesn't issue warnings. Skip workers comp and you're looking at:

Immediate Financial Pain:

Minimum $100 fine per day (yes, including weekends and holidays) once a stop-work order hits

Fines start accumulating the moment you're caught

Criminal Charges:

Up to one year in prison

Additional $1,500 fine

A criminal record that follows your business around

Business Shutdown:

Mandatory stop-work orders that halt your operations

You can't resume business until you prove you have coverage

Lost revenue, angry clients, damaged reputation

Massachusetts routinely issues stop-work orders resulting in tens of thousands of dollars in fines and extended shutdowns.

What Does Workers Comp Actually Cover?

When an employee gets hurt on the job, your workers compensation insurance Massachusetts policy kicks in to cover:

Medical Benefits

Full coverage for everything injury-related:

Doctor visits and specialist consultations

Emergency room treatment

Surgery and hospitalization

Prescription medications

Physical therapy and rehabilitation

All reasonable treatment necessary for recovery

No deductibles. No co-pays. No bills sent to your employee.

Wage Replacement

Injured workers receive approximately 60% of their average weekly wage while they're unable to work. The benefits adjust based on their situation:

Temporary Total Incapacity: 60% of wages during full recovery

Temporary Partial Incapacity: 60% of the wage difference if they return at reduced capacity (capped at 75% of full benefits)

Permanent Total Disability: Two-thirds of wages for life if they can never return to work

Important note: Benefits start after the first 5 calendar days of disability. These days don't need to be consecutive. If disability extends beyond 21 days, the first 5 days become payable retroactively.

Additional Coverage

Travel costs to and from medical appointments

Retraining assistance for employees who need to learn new skills

Reasonable accommodations to help them return to work

How to Get Workers Comp Coverage in Massachusetts

You have three options, though most businesses use the first one:

1. Private Insurance Companies

The standard route. We work with a licensed Insurer to get coverage tailored to your industry, payroll, and risk factors.

This is where working with an independent agency like G.Preto Insurance, LLC makes all the difference. We shop multiple carriers on your behalf: comparing rates, coverage options, and service quality: so you're not stuck with whatever one captive agent can offer.

At G.Preto, you get personalized service and a team that actually knows your name.

2. Massachusetts Workers' Compensation Assigned Risk Pool (MWCARP)

If you're in a high-risk industry and can't secure private coverage, the state's assigned risk pool is your backup. Rates are typically higher, but it ensures you can get compliant.

3. Self-Insurance

Large companies with deep pockets and strong financials can apply to self-insure. Must be approved by the DIA and meet strict financial requirements. This isn't realistic for most small to mid-size businesses.

Pro Tip: Once you have coverage, you must post your carrier's name in a common work area. Skip this and you'll face a $100 fine.

The Claims Process: What to Expect When Someone Gets Hurt

Accidents happen. When they do, the claims process follows a strict timeline:

Step 1: Employee Reports the Injury Your employee must report the injury to you immediately. Even if it seems minor, document everything.

Step 2: You Report to the DIA You have 7 calendar days (excluding Sundays and legal holidays) after the employee's 5th day of disability to report the injury to the Department of Industrial Accidents (DIA).

Step 3: Insurer Investigates Your carrier has 14 days to either begin paying benefits or issue a claim denial after receiving notice.

Step 4: Dispute Resolution (If needed) If there's a disagreement about coverage or treatment, the DIA handles mediation and hearings. Complex cases might require legal representation.

How to Keep Your Workers Comp Costs Down

Workers compensation insurance Massachusetts premiums aren't cheap, but you can control costs:

Review Job Classifications Annually Make sure employees are accurately categorized. Misclassifications can inflate your premiums or leave you underinsured.

Use an independent agent Rates vary significantly between carriers. An independent agency like G.Preto Insurance, LLC can compare quotes across multiple insurers to find you the best rate for your risk category.

Enroll in Safety Programs Many insurers offer premium discounts for businesses that participate in safety training and risk management programs. Fewer injuries = lower rates.

File Reports Promptly Late reporting can trigger audits and premium increases. Document injuries immediately and submit all required forms on time.

Work with a Broker Who Cares National carriers offer strong coverage options, but working through an independent agency ensures you have advocacy and access to multiple markets. At G.Preto, we offer complimentary insurance reviews to ensure your coverage still fits your business: and we look for savings opportunities every year.

Don't Navigate This Alone

Workers compensation insurance Massachusetts requirements are complex, penalties are severe, and getting the wrong coverage: or worse, no coverage: can sink your business.

That's where G.Preto Insurance, LLC comes in.

As an independent agency, we don't work for one insurance company. We work for you. We shop multiple carriers, compare options, and find coverage that protects your team without breaking your budget. You get personalized service, straightforward answers, and a partner who understands Massachusetts regulations inside and out.

Ready to get compliant or review your current coverage?Contact us today for a complimentary insurance review. Let's make sure your business: and your employees( are protected.) Email: gpreto@gpretoinsurance.com

Comments